The bull market for bonds has lasted for over 30 years—that’s an entire generation that has only known falling interest rates and favorable bond market returns.

Fixed income pundits have called for an end to this bull market run for several years now, but it hasn’t happened yet (at least not as of this writing). Interest rates today may be higher than they were at their lowest point of last year, but they really haven’t broken out to the upside as of yet. Certainly not enough to say the decades-long bond bull market is over.

But at some point, this run is going to stop and there will be a trend shift toward sustained rising interest rates. That’s why we believe the risks for bond investors are as high as ever in the current market environment. Many people see their bond holdings as conservative investments, but this mindset needs to change with bond market risks at their highest levels.

How did we get to this point? Let’s explore this question by looking at the role the Federal Reserve has played in lowering interest rates and raising risks for bond investors.

The Fed also rises

Prior to the creation of the Federal Reserve, bank runs and financial panics occurred frequently and randomly in the U.S. economy. There were the panics and subsequent recessions of 1857, 1873, 1893, 1907… you get the idea.

Many people, both inside and outside the government, recognized the need for greater stability in the U.S. financial system. Congress responded by passing the Federal Reserve Act, which was signed by President Woodrow Wilson in 1913. The law laid the groundwork for the establishment of the Federal Reserve System.

The Fed was created as a decentralized central bank in a compromise between the interests of powerful financial institutions and the needs of the general public for a solid and strong U.S. banking system. In its early years, the Federal Reserve worked to dampen volatility in the U.S. economy, especially during the Great Depression. Its mandate expanded to include open market operations and examinations of bank holding companies.

The Federal Reserve as we know it today would emerge in the early 1950s because of an agreement between the Fed and the U.S. Treasury related to interest rate pegs on government bonds. The federal government had borrowed significantly to finance the costs of World War II and the Korean War. Treasury officials wanted the Fed to keep interest rates low to support the war efforts, but central bankers were wary of the inflationary effects that “easy money” through unnaturally low interest rates could have on the U.S. economy.

The Treasury Accord, as it came to be known, gave the Fed more independence and entrusted the central bank with the ability to use the Fed funds rate as its monetary policy tool to guide the U.S. financial system.

The Fed flexes its power

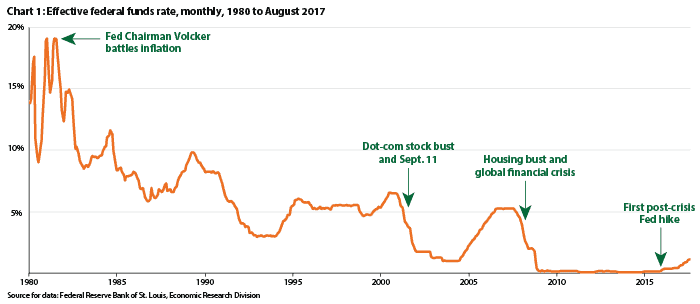

The Federal Reserve’s power would be put to its sternest test to date in the 1970s, as inflation strangled the U.S. economy. When Paul Volcker arrived to lead the Fed in 1979, he raised the Fed funds rate in less than two years to around 20%, seeking to bring inflation under control.

Volcker’s moves weren’t popular—his “tough love” approach to monetary policy raised borrowing costs for businesses, homeowners and the federal government in addition to contributing to the recession in the early 1980s. Ultimately, Volcker’s Fed won the battle: tighter monetary policy loosened the inflationary chokehold on the U.S. economy despite the short-term pain of higher interest rates. Inflation dropped from a peak of over 13% in 1979 to around 3% by 1983.

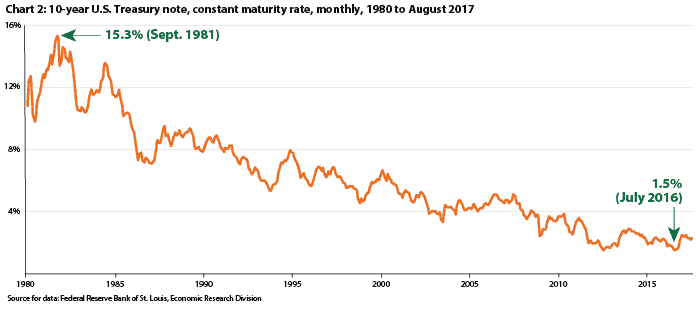

Having won the war against inflation, the Fed began to gradually lower the Fed funds rate in the mid 1980s to encourage U.S. economic prosperity. This sparked the decades-long decline in government bond yields—rates on 10-year Treasury notes would drop under the 10% threshold in 1985, under 7% in 1995, and under 5% in 2007(see chart below). The fall in bond yields naturally stoked a decades-long run for bond market bulls as well, one that really hasn’t ended as of the midpoint of 2017.

The Fed also had a hand in sustaining this bond market rally, lowering their target interest rate to near-zero in 2008 in response to the global financial crisis. The central bank also began an aggressive asset purchase program to help the U.S. financial system get back on its feet following the crisis. This level of monetary policy accommodation was unheard of in U.S. financial history, and it contributed to lofty price valuations for many asset classes, from stocks to real estate.

What does this mean for conservative investors?

From our current vantage point in 2017, we see interest rates that have risen from their lowest levels and appear to be on the way up. The Fed began raising rates in 2015, but the path to a tighter monetary policy has been a long and slow one. For example, in the previous tightening cycle the Fed raised rates over 400 basis points in about two years (July 2004 to July 2006). The current tightening cycle is already a year and a half old (December 2015 to July 2017) and the Fed has only hiked rates about 100 basis points.

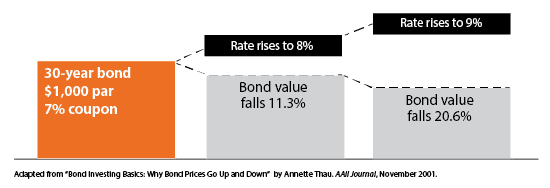

Astute investors are aware of the inverse relationship between interest rates and bond prices (i.e., rising rates decrease bond prices, and vice versa.) However, the math behind this relationship can be elusive. Investors need to understand how this dynamic affects the risk of bond investments.

Let’s take a simple example of a 30-year bond that has a $1,000 par value and a 7% coupon. As illustrated below, nominal interest rate increases of one and two percentage points can have drastic effects on the price of this bond. Declines of over 10% and 20% don’t seem very conservative.

Current rates on 30-year U.S. Treasury bonds are around 80 basis points higher now than they were last year at this time, so the risk of rising rates is real. In this type of environment, bonds should not be considered conservative investments and fixed income investors should consider alternatives.

How can Potomac help?

As a tactical investment manager, we have a handful of strategies for conservative investors to help minimize the risk of rising interest rates and falling bond values.

One of those strategies is our High Yield Plus program, which focuses on the tactical trading of high yield bonds. High yield bonds are often misunderstood by the general investing public, but when used properly they can complement nearly any investment strategy.

Historically, high yield bonds have demonstrated positive returns in rising rate environments. And by working with a tactical investment manager like Potomac, investors have access to a strategy that can help protect their assets in rising rate environment.

Disclosure: This information is prepared for general information only and should not be considered as individual investment advice nor as a solicitation to buy or offer to sell any securities. This material does not constitute any representation as to the suitability or appropriateness of any investment advisory program or security. Please visit our FULL DISCLOSURE page.